Serbian companies which apply International Accounting Standards and International Financial Reporting Standards (hereinafter: “IAS”/ “IFRS”) have a possibility to implement IFRS 15 – Revenue from Contracts with Customers as of January 1, 2018. This standard is the most comprehensive standard adopted over the last five years, and its implementation reflects through significant impact not only on financial reporting, but also on processes and information systems that should provide the required information in order to enable proper accounting treatment.

The underlying principle

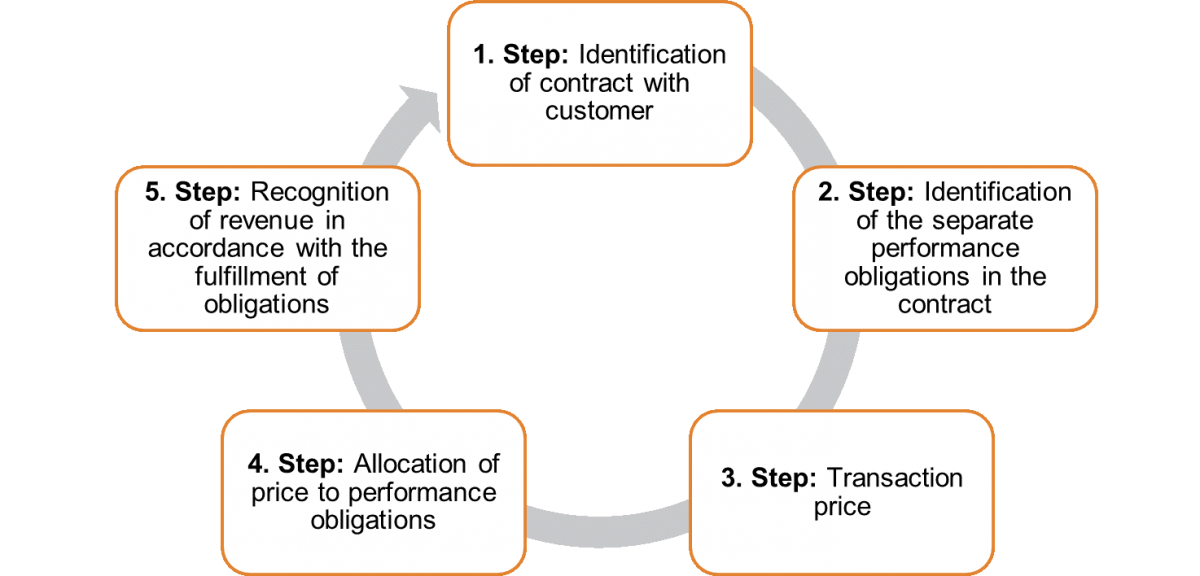

The underlying principle on which IFRS 15 is based is that income recognition is carried out in a manner that reflects the transfer of promising goods or services to customers in a value that corresponds to the compensation that a company expects to realize in exchange for those goods or services. Namely, income is determined and recognized by a model that implicates the implementation of the following five steps:

The application of IFRS 15 implies a significant effect on the financial reporting of certain types of companies, while for others it results in negligible adjustments.

The most affected sectors are:

- IT sector;

- Telecommunication;

- Cable operators;

- Construction;

- Auto-industry;

- Media;

- Pharmacy;

- Logistics;

- Retail.