1. Mandatory audits in Serbia

Audit of annual financial statements is mandatory only for certain legal entities. The deadline for signing an engagement letter for audit of financial statements for 2016 is 30 September 2016 or three months before end of business year to which the audit is related.

1.1 Audit of regular annual financial statements is mandatory for:

- large and medium sized companies,

- public companies (as defined by Law on Capital Market) regardless of their size,

- all legal entities whose operating income from the preceding business year exceeds EUR 4,400,000 in dinar equivalent and

- parent companies that prepare consolidated financial statements, that is legal entities that have control of one or more legal entities.

1.2 The deadline for signing an engagement letter for audit of financial statements for 2016 is:

- 30 September 2016 (for legal entities whose business year is the same as the calendar year);

- three months before end of business year to which the audit is related (for legal entities whose business year is different from the calendar year).

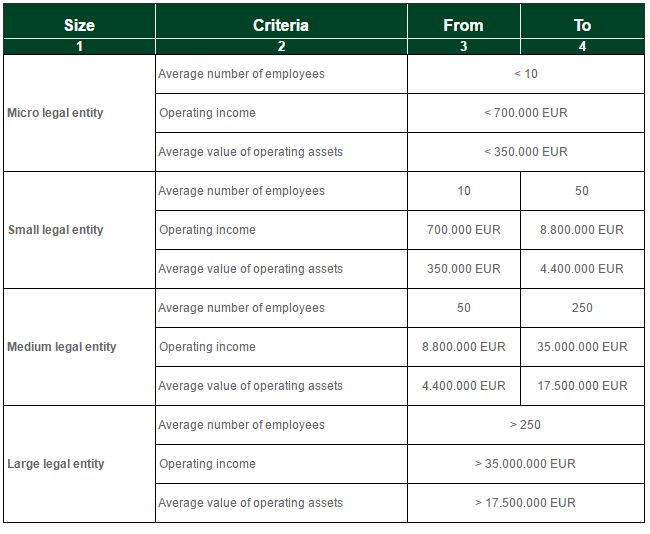

1.3 Legal entities are classified depending on the

- average number of employees,

- operating income and

- average value of operating assets

- Legal entities shall be classified as micro entities if they do not exceed two criteria listed in column 4 of the table.

- Legal entities shall be classified as small and medium entities if they exceed two criteria listed in column 3 of the table, but do not exceed two criteria listed in column 4 of the table.

- Legal entities shall be classified as large entities if they exceed two criteria listed in column 3 of the table.

Newly established legal entities shall be classified on the basis of data from financial statements for the year in which they were established and the number of months in business, and determined data shall be used for that and the following financial year.

Large legal entities

In accordance with the Law on Accounting, the following legal entities are considered to be large legal entities:

- the National Bank of Serbia (NBS),

- banks and other financial institutions supervised by the NBS,

- insurance companies,

- financial leasing providers,

- voluntary pension funds,

- companies managing voluntary pension funds,

- open- and closed-ended investment funds,

- investment funds’ management companies,

- stock exchanges and broker-dealer companies,

- factoring companies.

2. Application of standards in Financial Reporting

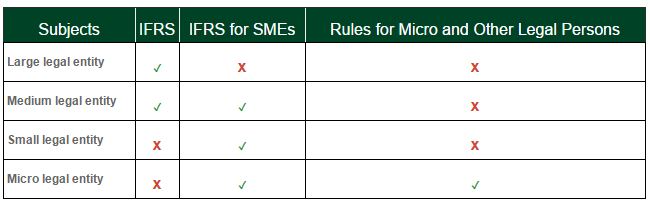

In accordance with the provisions of the Serbian Law on Accounting, large entities, parent legal entities, public companies, or companies that prepare to become public, in accordance with the Law on the Capital Market, shall apply International Financial Reporting Standards (IFRS), whereas small and middle entities shall applyInternational Financial Reporting Standard for Small and Medium-Sized Entities (IFRS for SMEs).

Micro and other legal entities, regardless of their size, shall apply Rules on the Manner of Recognition, Valuation, Presentation and Disclosure of positions in the individual financial statements of Micro and Other Legal Persons.

The law provides the possibility of choice in some cases, as shown in the following table:

Standards must be applied continuously. Thus, should a medium-sized legal entity decide to apply IFRS, it must apply IFRS until it becomes a small legal entity.

Do you have questions about IFRS or mandatory audits?

In addition to the audits of financial statements and special audits, TPA offers you expert knowledge in business consultancy and tax advisory. Our wide range of services include audit and advisory. We at TPA are committed to ensuring the highest levels of quality, and responsiveness in providing our services. Contact us!

Auditing services in Serbia

TPA’s Audit Approach

Our audit methodology is a “top-down”, operations risk focused approach, which, together with the use of technology, places it at the forefront of the current methodologies. Our audit approach encompasses the latest thinking on the use of controls and places significant emphasis on management’s role in controlling the operations.

In addition to understanding this role, the audit engagement partner and manager will invest time to understand the systems of your company and to tailor the audit plan by reference to the organization’s specific risk areas.

We will therefore focus our audit work on the way your company is managed and on those areas where issues are most likely to arise. Obviously, this methodology will enable us to direct our attention to those aspects of the operations which could significantly affect the financial statements, thereby avoiding unnecessary demands on your time and minimizing the disruption of your staff. Our operation risk audit methodology will leverage the risk assessment and controls that are already in place within your organization.

There are three phases in the risk assessment process:

- Assessment – We will work closely with the organization in order to analyse your current and future issues

- Implication – We will identify the potential impact of these issues on your financial reporting

- Focus – We will concentrate our audit efforts to address the key risks which will have been identified together with you

Our controls assessment also has three phases:

- Identification – We will identify the processes put in place by management to control each of the key risks, discussing with them how these procedures are carried out

- Alignment – We will assess the extent to which the control is effective in mitigating the identified risks

- Validation – We will then corroborate the control performance through rigorous validation and testing